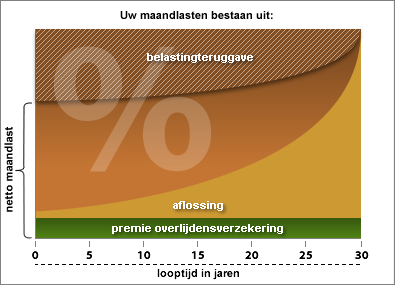

Of course, you simply pay interest on the mortgage you have taken out. In addition, you pay a small extra amount each year (or each month) as repayment. With an annuity, the total of that interest plus repayment remains the same. So you know exactly what to expect (provided that the mortgage interest rate does not change). Each year you repay a small portion of the mortgage debt. As a result, the amount of interest you owe also decreases each year. And that, in turn, creates room to repay a little more every year.

On top of that, the interest is tax-deductible. As a result, you pay less income tax: the “tax refund.” However, you will notice that this refund gradually becomes smaller over the years.